America First Credit Union Announces Winners of $5,000 Teacher Grant Contest

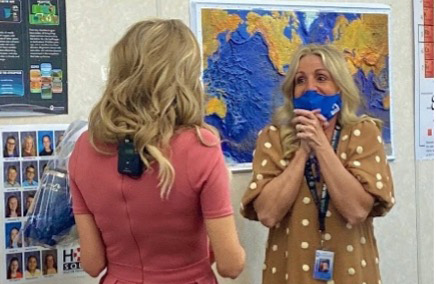

RIVERDALE, Utah – May 14, 2021 – America First Credit Union announced winners of the $5,000 grant awarded to ten K–12 teachers elevating youth financial literacy in Utah and Nevada. The grants will help fund projects for teachers. To wrap up Teacher Appreciation Week, May 3–7, America First Credit Union dropped by West Point Jr. High to surprise Kristy Larsen with a congratulatory announcement. The following teachers, who are using the free FUNDamentals financial literacy program in their classrooms, have received $500 grants: Utah Jacquelynn Merritt Lowder, Belmont Elementary, Alpine School District Mindi Barnes, Boulton, Davis School District Megan Barton,…